Two of the topics that raise the most doubts relate to Value Added Tax (VAT) and Personal Income Tax (IRS).

To give you a better understanding of these taxes, we answered some frequently asked questions below, because they are likely to change over the course of your business.

Under what circumstances is the TVDE driver exempt from VAT?

In a simple and summarised way, it can be said that the normal VAT regime applies to all self-employed workers who have a volume of activity greater than 15000 euros per year (amount already in line with the State Budget for the year 2026). And that, if the turnover is less than €15000 per year, does not have organized accounting, or carries out imports or exports, it will be covered by the exemption regime.

This means that TVDE couriers/drivers are exempt from VAT if they are starting their activity and do not have or are required to have organized accounting and do not expect to reach a turnover of more than €15000 in the current year.

The communication of the expected turnover is made through the declaration of commencement of activity delivered to the Tax Authority.

VAT exemption is maintained in the following years as long as they have not reached, in the previous calendar year, a turnover greater than €15000.

Under what circumstances does the TVDE courier/driver switch to the normal VAT regime?

The TVDE courier/driver is exempt from VAT in the first year (as long as they do not expect to reach a turnover of more than €15000) and remain in this regime if they do not exceed this limit. If this limit is exceeded, the TVDE courier/driver will revert to the normal VAT regime.

It should also be noted that if the limit of €15000 in income is reached at a certain time of the year, the TVDE/courier driver only has to start charging VAT in January of the following year, submitting a declaration of change of activity to finance (via the Finance Portal or in person at a finance desk).

If you choose to submit the declaration online:

1. Log in to the Finance Portal

2. On the side menu of the main page, click on “All Services”

3. Click on the “Activity Change” section

4. Click on “Deliver statement”

5. On the new page, click on the button “Submit declarations”

6. Fill in the declaration fields,

7. After filling in all the fields, click on the “Validate” button

8. A pop-up window will appear with the summary of the filled in data. If everything is correct, click on the “Ok” button.

9. Submit the statement by clicking on the “Submit” button.

Under what circumstances the TVDE courier/driver don't need to make withholding tax?

In short, it can be said that self-employed workers who have received category B income of less than €13,500 in the previous year, or who anticipate not exceeding that amount during the year they start their activity, are not obliged to withhold at the IRS source.

Some important aspects:

➔ The threshold of €15000 is the same as that defined for VAT exemption.

➔ Exemption from withholding is optional.

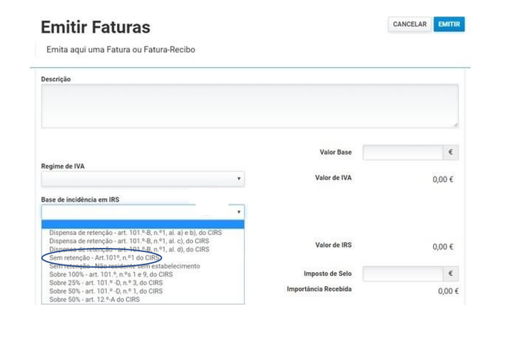

➔ It is essential that IRS withholding waiver holders (and those who wish to take advantage of this same exemption) do not forget, when issuing invoices on the Finance Portal, to effect this withholding waiver.

They must do so by selecting, in the “IRS tax base” field, the option “Without withholding - Art. 101, nº 1 of the CIRS”.

➔ The exemption extends to the following years if, in the immediately preceding year, the taxpayer has not earned income equal to or greater than the established limit.

Under what circumstances does the TVDE courier/driver start withholding IRS?

With regard to the IRS, the TVDE courier/driver is subject to mandatory withholding tax when the activity amounts to annual billing amounts equal to or greater than €15000.

It should also be noted that the exemption ends in the month following the month in which the fixed limit is exceeded. That is, if the TVDE/courier driver exceeds the value of billing of €15000, at a certain time of the year, on the next receipt you have to start withholding IRS.

Notwithstanding the information provided, we are not responsible for any misinterpretation and we advise you to always follow up your case with an accountant since all the tax issues under analysis are constantly changing.